Program Overview

MCC’s $475 million Burkina Faso Compact (2009-2014) included the $6.8 million Access to Rural Finance Activity which sought to improve access to rural finance through the creation of a loan fund, as well as capacity building to participating financial institutions and farmers. The activities were based on the theory that by improving the quality of farmers’ loan applications and banks’ ability to evaluate them, banks would increase the number of loans made to farmers. Farmers in turn would increase their agricultural productivity, generate higher incomes and thereby reduce poverty.

Evaluator Description

MCC commissioned A2F Consulting LLC to conduct an independent final performance evaluation of the Access to Rural Finance Activity. Full report results and learning: https://data.mcc.gov/evaluations/index.php/catalog/150.

Key Findings

Rural Lending Outcomes

- Rural lending did not expand as a result of the activity.

- The loan fund, intended to serve as a stable, long-term source of funding for banks, was insufficient to incentivize banks to expand rural lending.

Loan Assessment Outcomes

- Despite capacity building, banks did not adopt new methods and tools for assessing rural lending. The methods and tools were intended to mitigate the perceived risks and costs of rural lending.

- Banks continued to assess farmers’ loan applications in the same way as regular loans, such as by requiring collateral, which prevented many applicants from obtaining a loan.

Business Training Outcomes

Evaluation Questions

This final performance evaluation was designed to answer the following questions.

For banks:

- 1

Did banks receive more or better-quality applications for rural agricultural loans? - 2

How, if at all, did banks change their practices for rural lending? Did the program succeed in changing banks’ risk perception of rural lending? - 3

Did banks increase their portfolio in agricultural investments? Have non-participating banks begun to invest more in agriculture?

For farmers:

- 4

Did farmers receive credit at a higher rate? - 5

Did farmers increase their business management capacity?

Detailed Findings

These findings build upon the interim evaluation report results published in 2016.

Rural Lending Outcomes

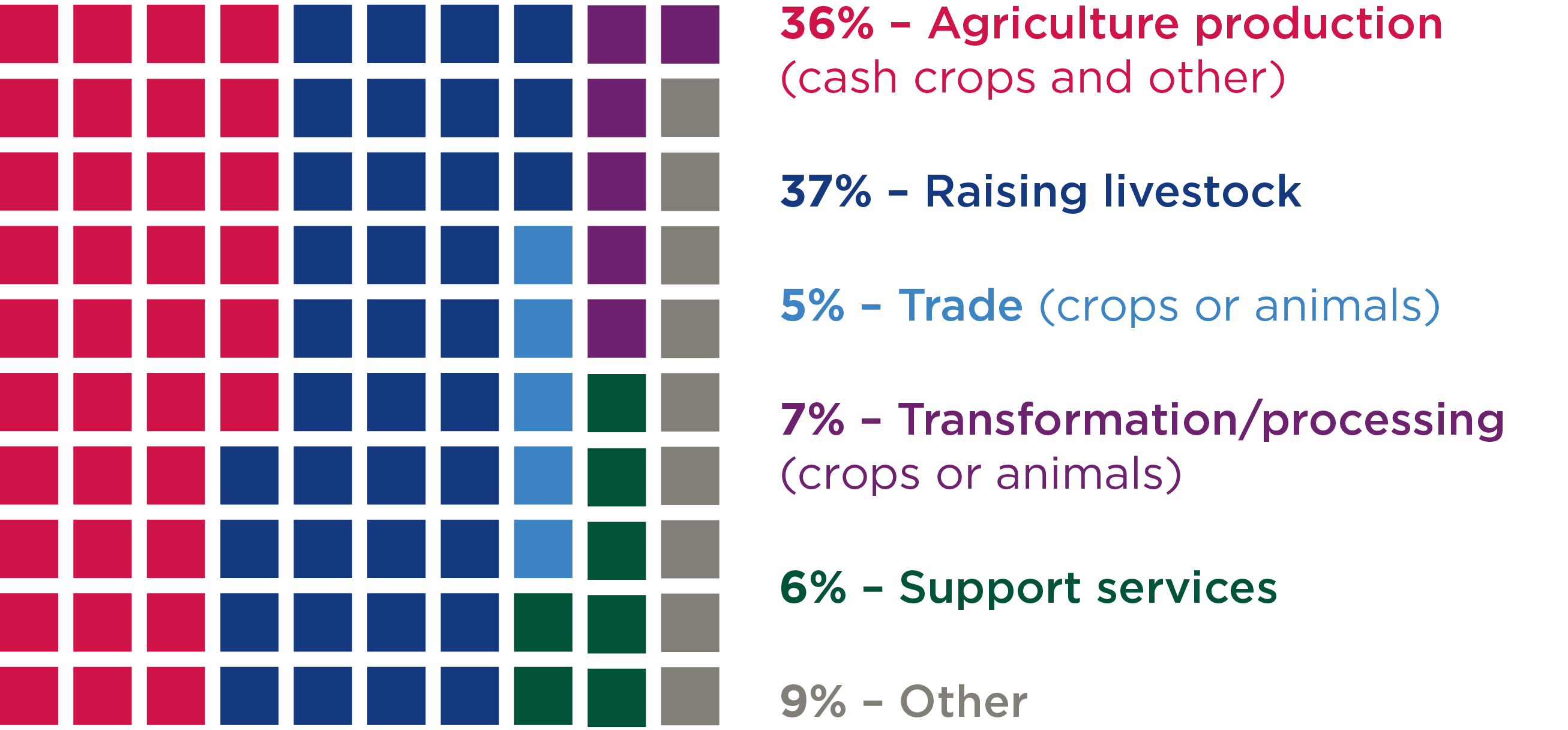

Final beneficiaries sample by business sector

The Access to Rural Finance Activity did not translate into banks approving more loans to farmers. The loan fund did not sufficiently incentivize banks to expand their rural lending portfolio or change their lending practices. While banks received funds at the below-market, concessional rate of 3%, this did not adequately compensate banks for the risks and additional administrative burden of rural finance. As a result, only one out of the three participating banks significantly utilized the available funds. Ultimately, the loan fund was only able to disburse $2.8 million in loans compared to its initial target of $10 million.

Of the 68 loans that were disbursed under the activity, a sizeable amount of loans did not go to agricultural production (the activity’s target) but rather business-related agricultural transformation, such as oil production.

Loan Assessment Outcomes

Banks did not adopt new methods and tools for assessing rural lending as a result of capacity building. While some bank staff members found the training useful, others found the training time-consuming, too theoretical, and lacking proper follow-up and refreshers. Delays in project implementation and cumbersome administration also contributed to the issue, and ultimately banks stopped actively promoting rural loans. MCC’s decision not to include a risk-sharing mechanism to incentivize banks to change their loan assessment criteria left MCC without strong leverage to alter their lending practices. As a result, banks continued to assess farmers’ loan applications in the same way as regular loans, and farmers did not enjoy enhanced access to rural finance.

Business Training Outcomes

In total, 170 farmers, farmers groups, and agro-businesses received business training as part of the activity. The business training was intended not only to reinforce farmers’ capacity to prepare successful loan applications, but also to improve their management practices to increase their ability to pay back the loan. A major potential synergy of the activity – to provide business management training to farmers who would prepare better loan applications that banks would then assess using specialized rural finance criteria – did not materialize. The capacity building component did not succeed in altering banks’ loan approval criteria to better address the needs of farmers seeking rural financing, and banks simply continued to assess these loans in the same manner as regular loans. Banks reported that loan applications the farmers produced as part of the business training were of poor quality and had unrealistic business plans.

Farmers also complained about the quality of the business training provided by the activity. In qualitative interviews, over half of farmers said that the quality of business training was either “poor” or “very poor.” Almost half of farmers interviewed received loan application documents or assistance on action plans, and just 13% received training. Specifically, farmers complained that trainers did not inform them of capital requirements; did not update the farmer on the status or result of their application; or submitted the farmer’s application to banks not involved in the Access to Rural Finance Activity.

MCC Learning

A thorough needs assessment must be completed to ensure that: 1. The needs and capacities of sector actors are considered, 2. Incentives are properly aligned across sector actors, and 3. Incentives are sufficient to bring about the project-required outputs.

Consumer protection safeguards should be put in place to avoid potential abuses and/or the provision of misleading information to end users.

Specific, sector experts need to be hired; both by MCC and by the MCA in order to provide sufficient oversight and direction.

Evaluation Methods

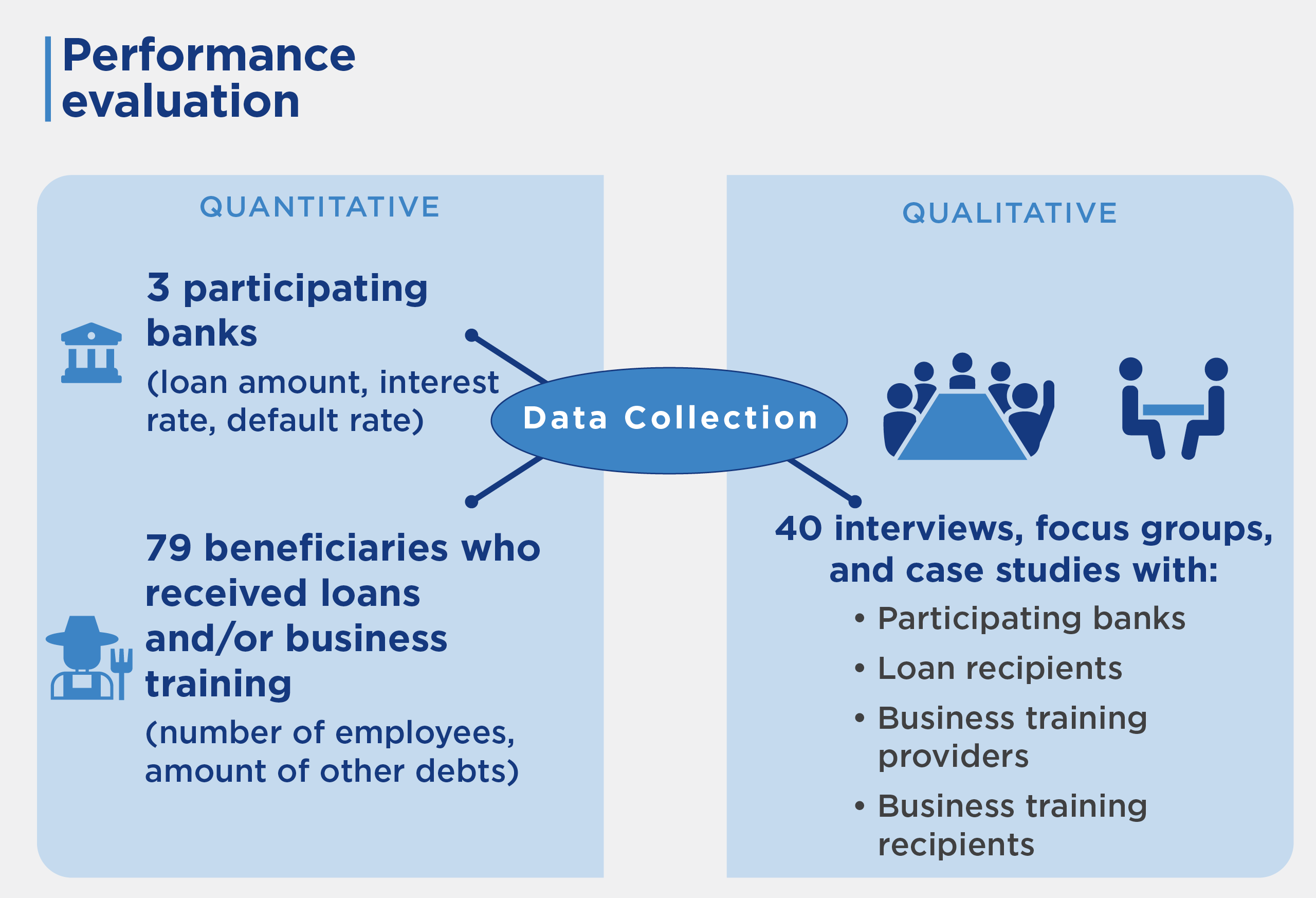

The activity was evaluated using a rigorous mixed-methods performance evaluation approach with an ex-post thematic analysis methodology. The evaluation focused on examining project design, implementation, outcomes, and lessons learned. Data collection was conducted over a four week period in April and May 2015. There were four key groups targeted for data collection: participating banks, business development providers, business development participants, and loan recipients. Depending on the group the evaluation team used quantitative financial data, semi-structured interviews, surveys, focus groups, and case studies.

Quantitative data was collected from the three participating banks (e.g., loan amount, interest rate, default rate) and supplemented with information on agricultural lending from the Central Bank of West African States. In addition, 13 management staff from two of the participating banks participated in semi-structured interviews. For the business development providers 10 participated in semi-structured interviews. The evaluation team surveyed 79 of the business development participants and convened two focus groups, while the team surveyed 30 loan recipients along with two focus groups and five case studies.

Due to significant delays, the Access to Rural Finance Activity did not become fully operational until early 2013, almost four years after compact signing, and two and a half years after the expected start date. Due to limited uptake of various Access to Rural Finance services and the low likelihood of the activity achieving its intended goals, the activity was discontinued in 2014, one year before the end of the compact. The evaluation data was gathered in 2015. By then, banks had accessed the loan fund for two years, and farmers had accessed business training services for six months.

2022-002-2691