Program Overview

MCC’s $547 million Ghana Compact (2007-2012) funded the $30 million Financial Services Activity which aimed to establish a computerized networking system among 130 rural banks and APEX, the bank regulator. The system was designed to improve financial service delivery, operations, and access to information at rural banks with the objective of enhancing the depth, value, and reliability of rural financial services, and widening access to savings services and cash transfers for rural communities.

Evaluator Description

MCC commissioned NORC at the University of Chicago to conduct an independent final impact evaluation of the Financial Services Activity. Full report results and learning: https://data.mcc.gov/evaluations/index.php/catalog/192.

Key Findings

Transaction Speed and Reliability

- Rural banks reported that the average transaction time decreased from 15 minutes to less than 5 minutes, and in some cases to as low as 2 minutes.

- Reduced waiting time and faster service greatly improved the customer experience.

Accuracy and Availability of Accounts Information

- Rural banks indicated that real time monitoring of branches through the connectivity system greatly improved bank supervision and resulted in reports that were more accurate compared with before the project.

- The activity had a positive effect on the value of accounts and average balances per customer, which is consistent with the improved customer experience.

- The activity had a positive effect on bank net income; however, bank expenses per customer have not changed.

Transaction and Check Clearing Times

Evaluation Questions

This final impact evaluation was designed to answer the following questions.

- 1

Did the activity improve the speed and reliability of transactions? - 2

Did the activity improve accuracy and availability of accounts’ information? - 3

Did the activity reduce transaction times and check clearing times?

Detailed Findings

Transaction Speed and Reliability

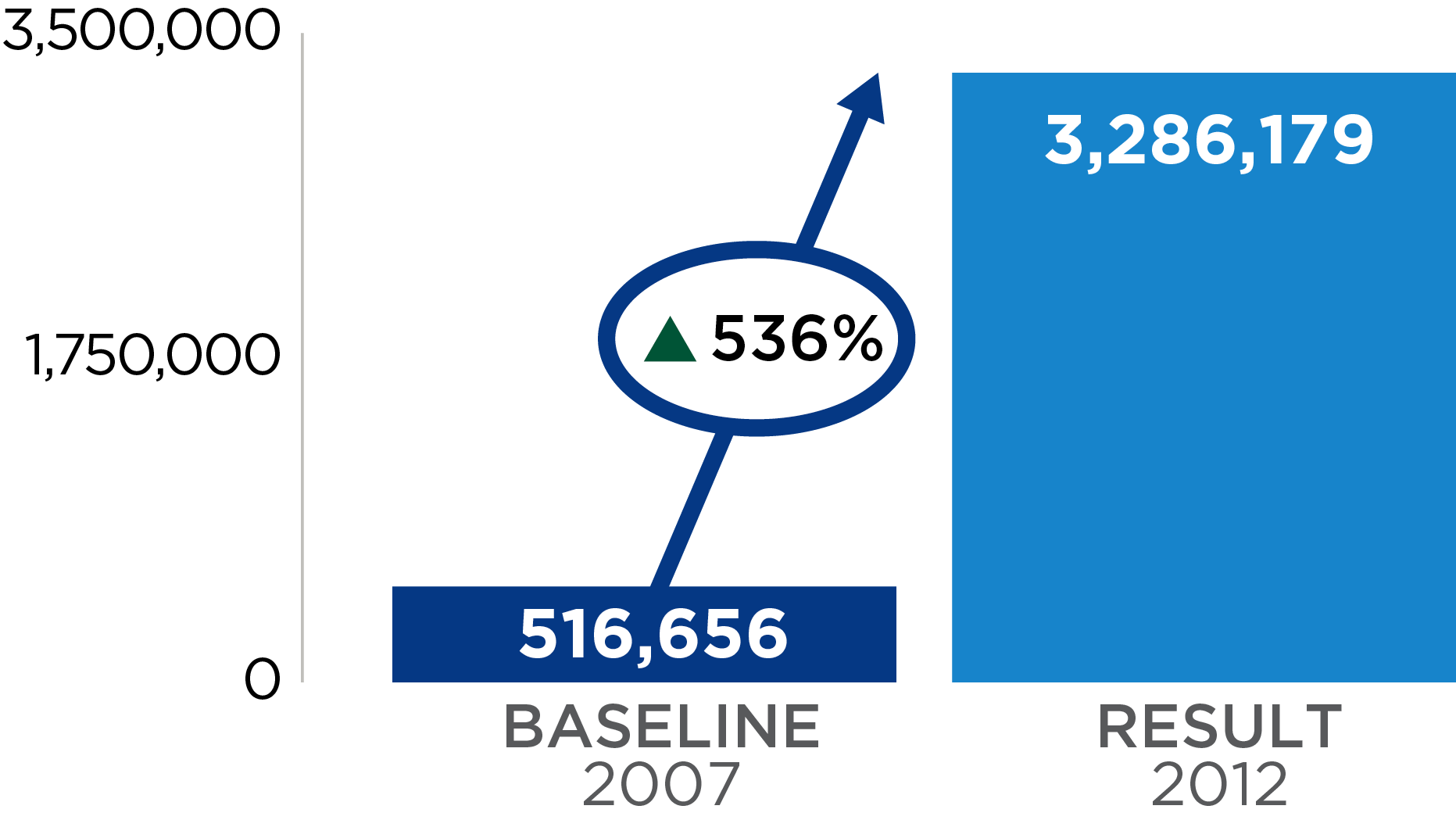

Number of inter-bank transactions

Banks and their clients reported an improved customer experience because of the reduced waiting time and faster service. All rural banks indicated the average transaction time lowered from 15 or 20 minutes at baseline to 5 minutes or less. Some banks also reported a reduction in check clearance time from up to 5 days to 1 day. Waiting time only exceeded these times at the end of the month when many people collect salaries or pay school fees. Most rural banks agreed that the i-transfer system (the inter-rural-bank transfer of funds), was a major upgrade to the previous telephone system.

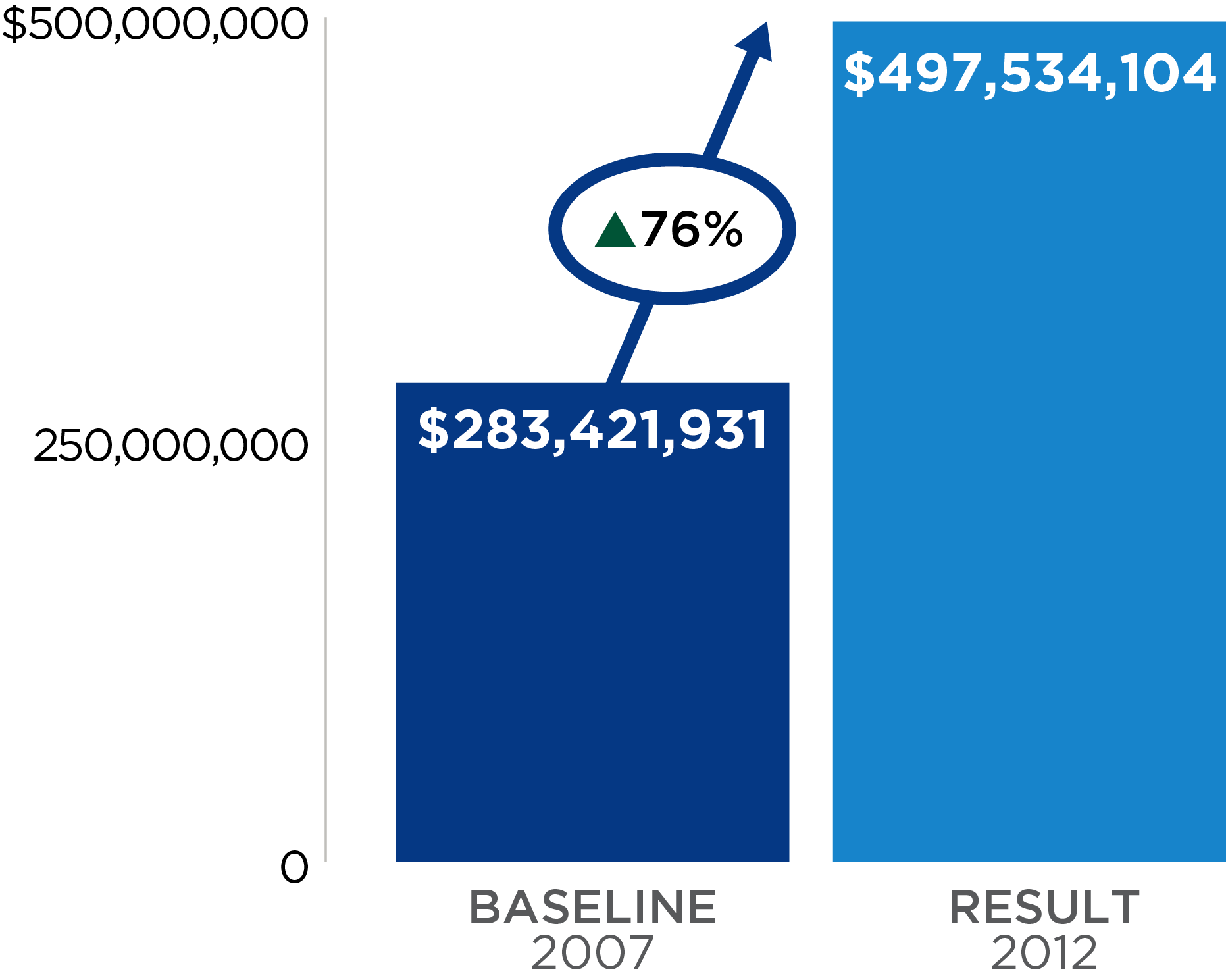

Value of deposit accounts in rural banks

The value of accounts and average balances per customer increased, although the number of customers was not affected, indicating a possible improvement in the customers’ satisfaction that could be linked to speed and reliability of bank services. The number of inter-bank transactions increased exponentially from baseline to endline, which was an expected medium-term result.

Accuracy and Availability of Accounts Information

The rural banks reported that real-time monitoring of branches through the connectivity system has greatly improved supervision and the accuracy of reporting compared with before the project. Relatedly, the rural banks visited concurred that they are now more confident about the security of their data, and feel assured that the information technology (IT) upgrades will keep their data safe in case of disaster.

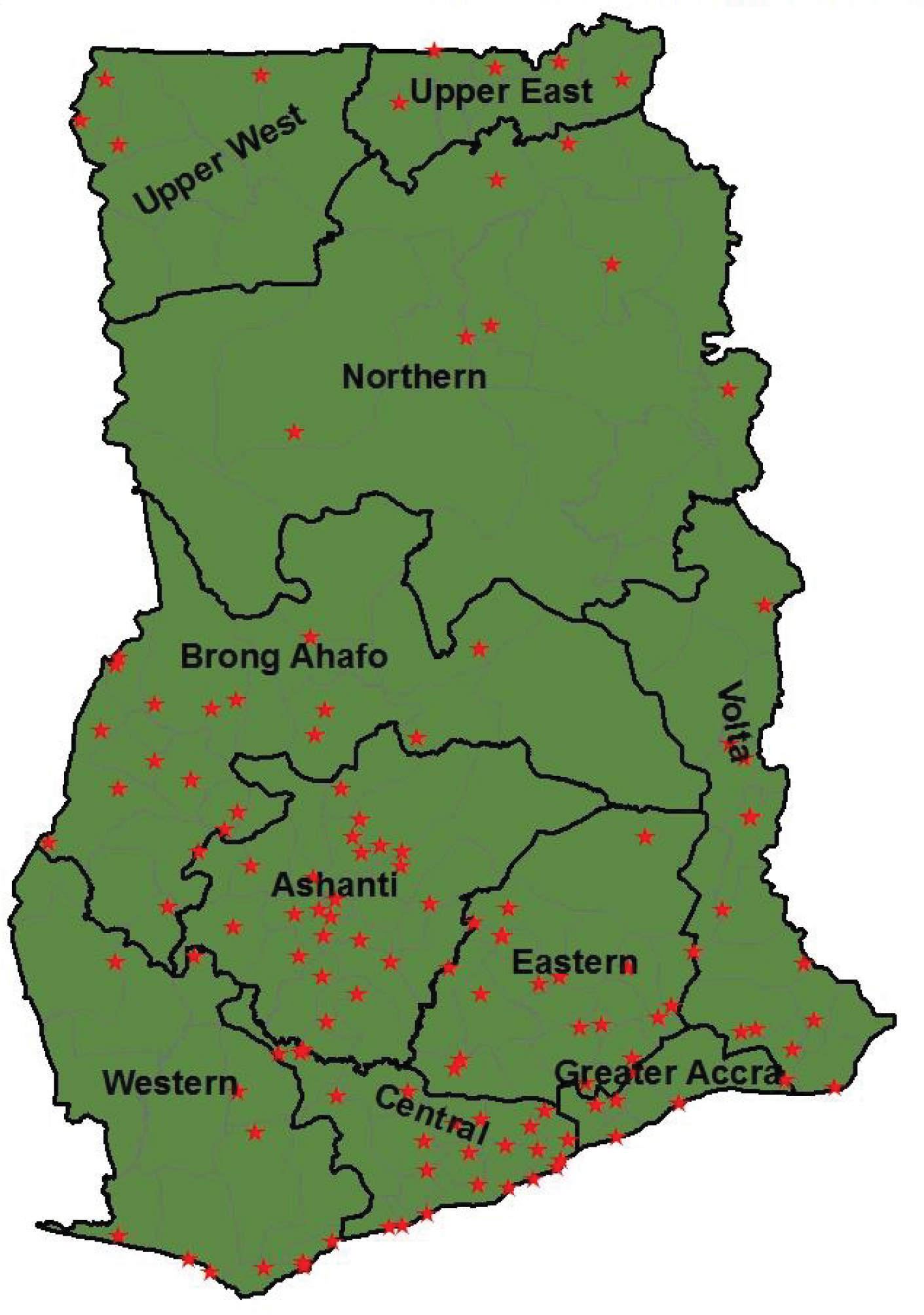

The 130 Ghanian rural banks in the activity

More accurate bank statements improved the customer experience, and bank clients who were interviewed confirmed this finding. In interviews with key management at select rural banks, the majority agreed that customers have overall gained greater confidence in dealing with them, and their reputation has greatly improved compared with the pre-project period.

Results show a positive effect on the value of accounts and average balances per customer (change in the value of deposit accounts for baseline and endline depicted in figure), which is consistent with improvements in the customer experience. The evaluation also found a positive effect on bank net income; however, bank expenses per customer have not changed.

The project had a strategic impact in convincing the rural banks to embrace information technology and its implications and generated a growing appetite for learning and adopting modern technology for their operating needs. After the intervention, rural banks expressed interest in more sophisticated and diversified IT products such as ATMs, internet banking, and integration with mobile money, which assure seamless and uninterrupted services.

Transaction and Check Clearing Times

Being connected to the national check clearing platform, Check Codeline Clearing, vastly improved check clearing times. Additionally, electric generators, provided to all rural banks experiencing power outages, helped them to continue operating even with electric power interruptions, thereby maintaining reduced transaction times.

However, there was little anticipation of the volume of data growth after implementation, and operating costs were not fully taken into account. Software licensing and communication fees rose substantially to an unaffordable level, primarily because of the major devaluations (more than 100 percent) of the Ghanaian currency, which resulted in doubling of fees associated with a US dollar-based contract. Initially, a Data Center and disaster recovery facilities were built and commissioned to ensure infrastructure connectivity. Two years after the end of the project, the Data Center became obsolete and had to be replaced with a new server to accommodate data growth. The project originally issued software licenses (with a regular cost of about $1,500 USD per user) free of charge to the banks, but because of subsequent rapid growth, they did not have enough user licenses. This left some staff, such as loan officers, without a user license and caused inefficiencies.

MCC Learning

Future projects should anticipate an increase in the volume of data after implementation, and estimate costs and required resources appropriately.

Product development can be a major source of growth for rural banks. Structural arrangements or relationships that hinder product development can limit rural banks’ growth. Future projects should incorporate a certain degree of autonomy for individual financial institutions.

Evaluation Methods

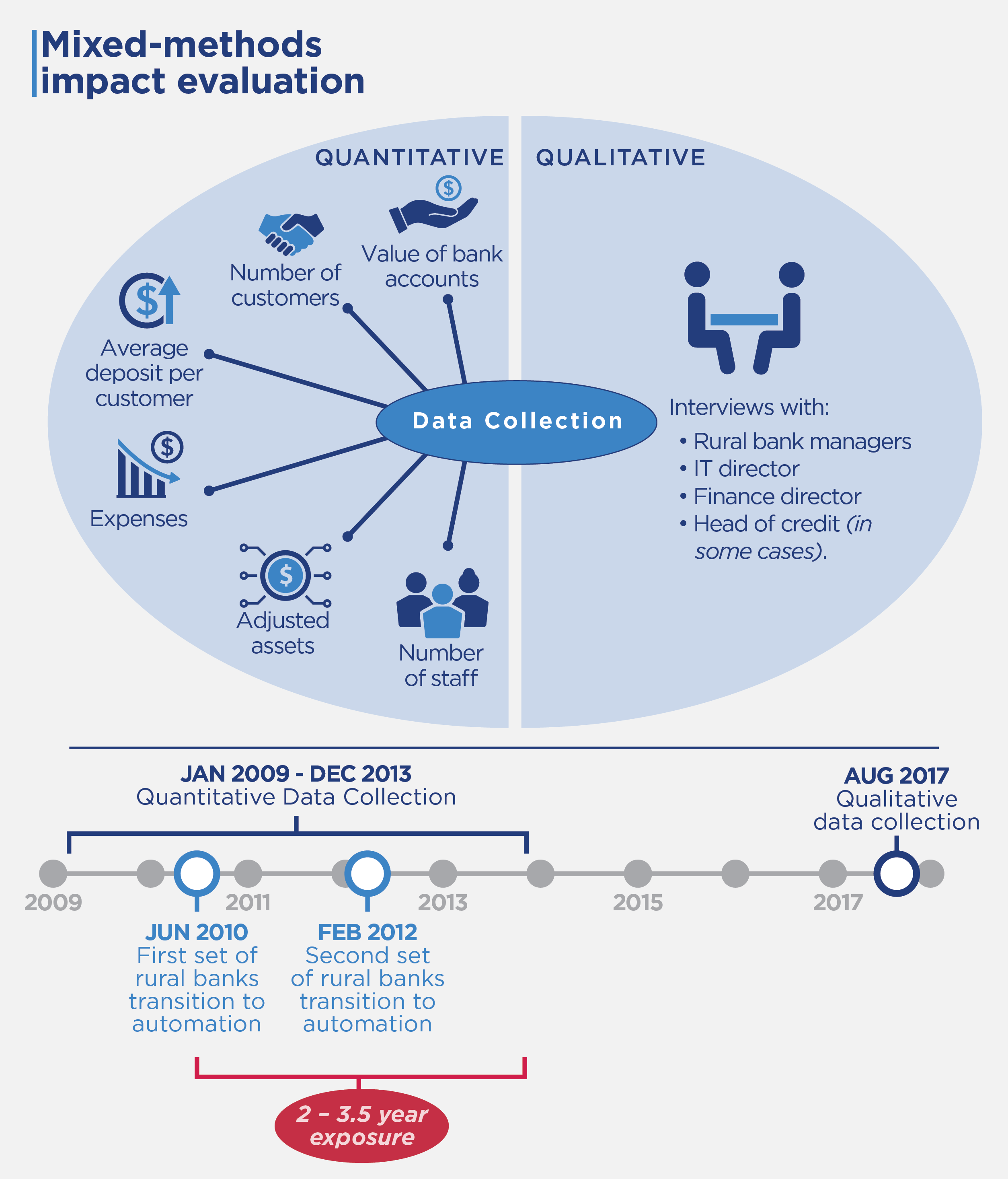

The study used a mixed methods impact evaluation, including quantitative and qualitative information, to estimate the impact of computerization and connectivity on several key bank performance indicators. The rollout of the intervention across banks was staggered over a 20-month period. The first rural banks made the transition to automation in June 2010, and the final set of rural banks completed the process in February 2012. The staggered rollout of the intervention allowed the evaluator to use longitudinal bank data to identify and measure the activity’s effects relating to the value of bank accounts, number of customers, average deposit per customer, expenses, adjusted assets, and number of staff.

Quantitative data spans the period from January 2009 (16 months before the first set of rural banks was computerized) to December 2013 (almost two years after the intervention ended), allowing for an exposure period of between nearly 2 years and 3.5 years. Panel data was analyzed using ordinary least squares (OLS) and fixed effects regressions.

The qualitative study examined bank managers’ perceptions about the activity and performance trends with the aim of better explaining the activity’s impact. Data was collected in August 2017 at 14 rural banks, more than five years after the compact closed. Data collection included interviews with rural bank managers, the IT director, the finance director, and in some cases, the head of credit. In selected banks, the team interviewed three customers (male and female), when possible.

2021-002-2567